How We're Allocating Our Money

Assessing assets to weather changing tides and raucous waves, while seeking shelter from approaching storms. A periodic portfolio review.

Atlanta, GA

August 5, 2024

“Scared enough to save for the short-term, brave enough to invest for the long-run.”

- Morgan Housel

The first thing most people do in situations like this is panic. So at least they’re doing it in the right order.

But we’ve had a plan and are sticking to it. This morning, markets tanking again. The yen carry-trade is rapidly unwinding.

Overnight, the Nikkei fell more than 12%…the biggest decline since the ‘87 crash. In the US, indices opened down 4-6% (tho’ as often happens, they’ve alleviated some losses after the “amateur hour” following the morning bell).

Who knows how long the drops will continue or how far they’ll go? That’s the only answer that’s easy:

No one. Especially us.

We’ve simply taken precautions to balance our vessel and stay afloat. Today, we take extended time to divulge what they are.

Taking Inventory

Clouds are darkening and waves are rising. Riding a leaky economy on rough seas, we take inventory of what’s needed to survive the approaching storm.

Among the essentials are a compass, and a calendar. Shadows lengthen across the market. We know not the hour. Yet we need a sense of the season, and the direction we’re headed.

Markets, like lives, have reliable cycles…and distinct times. These will guide us as we decide what to retain as we sail to safety.

In this phase of the market and stage of our lives, our objective isn’t to “get rich”. It’s to not become poor.

With that in mind, we’re fine forgoing short-term gains to elude large-scale losses. To stay afloat, we’ve compiled a portfolio of assets. Among them is a dwindling allocation to stocks, for which stop losses are a lifeboat when the winds kick up.

As with anything, trailing stops have their risks. Sometimes they’ll throw us overboard just as the sea subsides.

But as darkness descends and barometric pressure drops, I’m fine forgoing a rising tide if it means avoiding an iceberg. I want to board our vessel with eyes wide open, and with one on the exits.

Before we stock the galley, let’s clear the deck. The first item overboard is…

Bonds

With the exception of short-term T-bills (which I categorize as “cash”), we’ve been reluctant to hold bonds. Not that they can’t be a good tactical trade, particularly after yields spiked the last couple years…or if investors rush to cash their chips after other bets go sour. But with the casino in shambles and the croupier in decline, I’ve preferred to stay away from the table.

For forty years, the tide came in. Stocks and bonds rose together on an ocean of credit. But as the current shifts, the undertow strengthens. When rates rise, stocks and bonds struggle to stay afloat.

In 2022, the “60/40” portfolio by which they’ve been tied together sank further than it ever has. Since then, it’s come up for air, albeit buoyed by a small cohort of the strongest swimmers.

Bond yields move in generational cycles. They fell precipitously after the First World War, and rose relentlessly after the second. They didn’t peak until many of the surviving soldiers had full-grown grandsons.

After the early ‘80s they doggedly dropped. A few years ago, they scraped 5,000 year lows. But now they’ve escaped the channel down which they slid. As the wave again begins to rise, bonds could become less a life vest than an anvil.

Bond risk comes in three forms: default, currency, and interest rates. An explicit default on US government debt is extremely unlikely. Instead, lenders will suffer a stealth heist, with inflation wielded as a surreptitious weapon.

As rates rise in response to that risk, bonds lose value over time…as we’ve seen the last couple years. And principal is returned in deeply depreciated currency.

This won’t happen in a straight line. At the moment, sentiment is stretched and rates are liable to drop. The Fed signaled as much last week, indicating rate cuts could be on the near horizon, perhaps hitting the radar as soon as September.

That isn’t a harbinger of health. Reductions in the fed funds rate don’t usually interrupt recessions. They announce them. But last week came a more reliable sign.

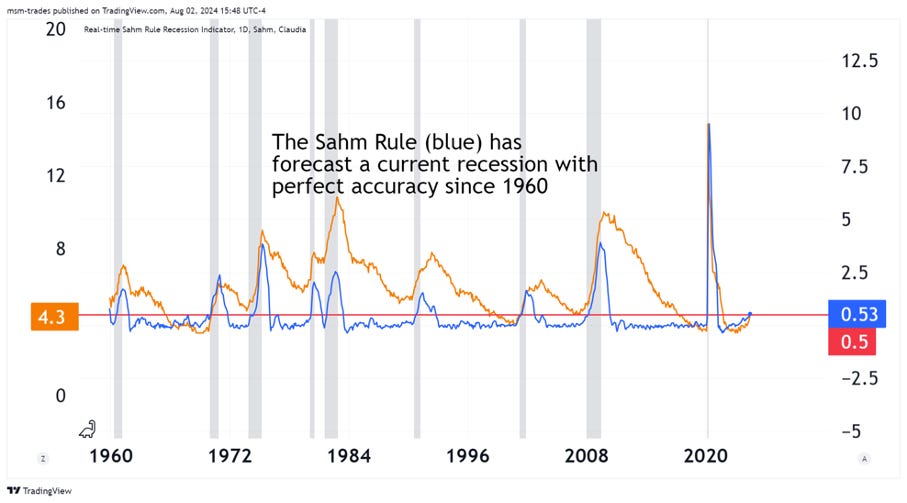

According to the Sahm Rule, when the average three-month unemployment rate rises half a percentage point over the lowest three-month average of the previous year, the economy is in recession.

As the chart above reveals, the Sahm Rule (red line) hasn’t given a false alert since 1960. A July unemployment reading (orange line) of 4.2% would’ve sent the signal. Friday, it registered 4.3%. And the labor market is usually a lagging indicator.

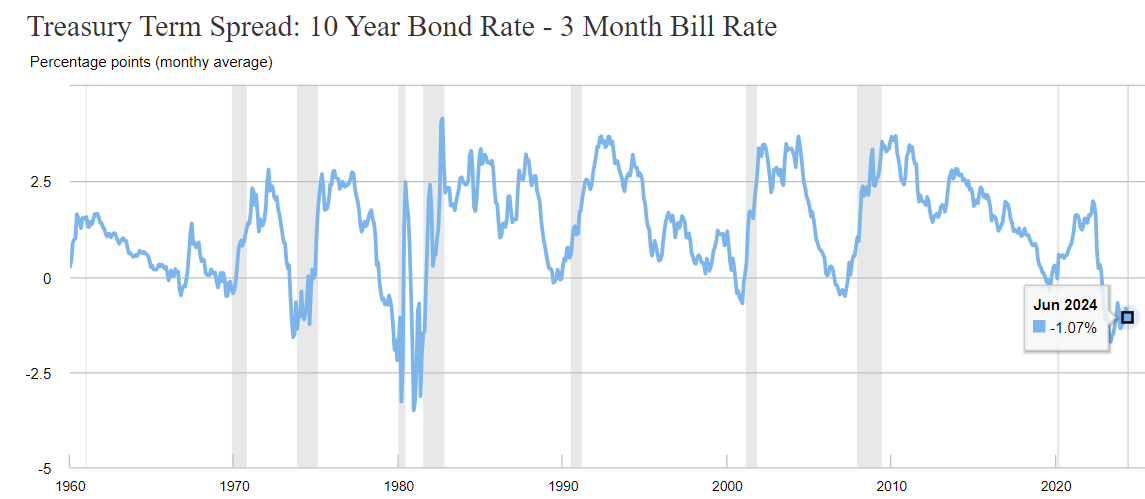

The yield curve is a leading one. For two years its been inverted, a near flawless gauge of upcoming contraction.

But the economy usually doesn’t slump while the curve is flipped. The carnage comes after yields resume their accustomed configuration. That hasn’t happened yet, but it’s inching closer.

If the economy tanks, stocks could drown. They’d probably pull yields down with them as money seeks support from “safe haven” bonds.

But will it be swimming toward the eye of the storm? Treasuries can be a temporary dinghy when the tide goes out. But if a tsunami comes in, that rickety raft can quickly go down. I’d rather not be on it at all.

Gold

Now that we’ve plugged a hole, let’s assess our anchor.

Gold performed exceedingly well during the 1970s, the historical period we seem destined to revisit. It also outperformed stocks during the first two decades of this century.

While the S&P 500 has nearly quadrupled since 2000, gold is up almost nine-fold. Gold fetches seventy times as many dollars as it did when the two were tethered. Stocks are up “only” fifty times (including re-invested dividends) since the gold window was closed.

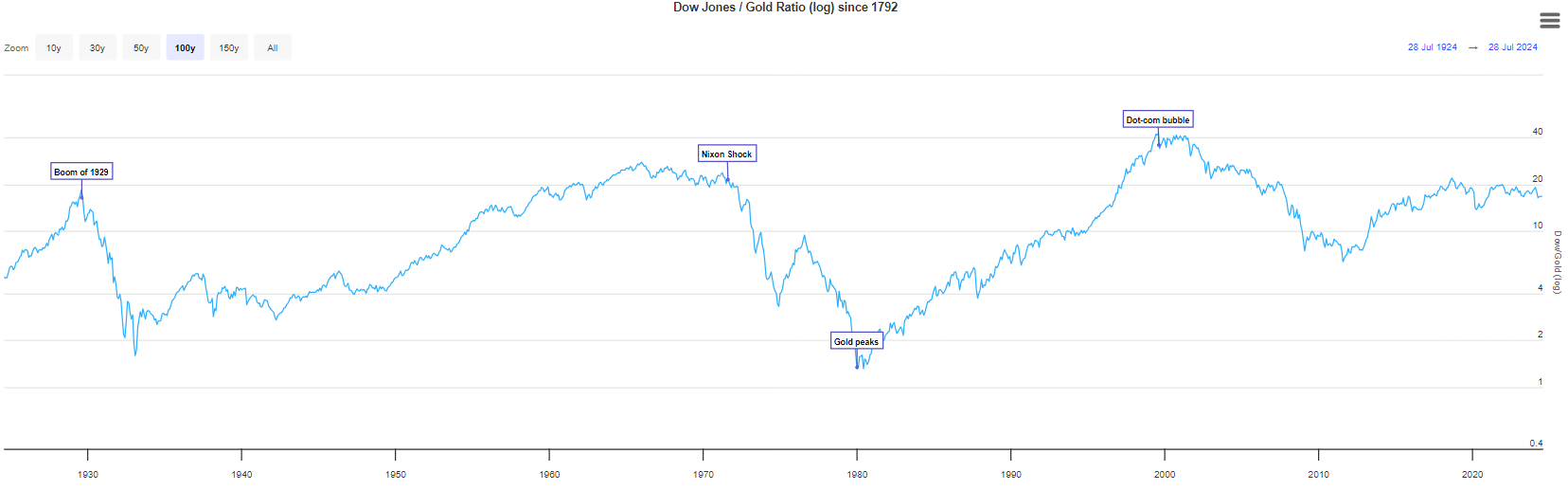

One of the crucial cycles we’ve previously referenced is the “Dow-to-Gold ratio”. Bill Bonner and Tom Dyson employ this measure…merely the Dow Jones Index divided by the price of an ounce of gold…as their compass. It uses real money to smooth out inflationary “noise” and better assess the value of stocks. When the ratio is high, stocks are expensive; when it’s low, they’re cheap.

This tool isn’t to “time the market” or be too precise. As Bonner put it, we’re not trying to hit the apple; we just want to ensure William Tell is pointed in the right direction.

The Dow peaked in 1929 at about 18 ounces of gold. That was the time to sell stocks, and accumulate more of the Midas metal. A few years later, the ratio tanked to below two…a signal to exchange holdings of gold for inexpensive stocks.

For almost forty years the Dow climbed, exceeding twenty ounces in the late 1960s. The bell was ringing, and the top was in. Those who swapped stocks for gold avoided an 80% inflation-adjusted decline during the 1970s.

By the end of the decade, stocks were shunned, the Dow-Gold ratio approached one…and it was time to buy. For twenty years, the Dow went on a record run, and gold fell asleep (or into a coma). At the turn of the century, the ratio crested forty.

Everyone was in love with stocks, and disparaged gold. It was time get out of the market, and run for shelter. But few wanted to turn off the music or close the bar. Finally, in March 2000, the cops showed up. And over the following two years, nausea intensified as the hangover hit.

Except for those who sold stocks for gold before the sun set. While stocks trudged higher into the ’08 financial collapse, gold multiplied four-fold. After the meltdown, the Dow-Gold ratio had fallen to six.

Then, for the next twelve years, the pendulum swung the other way. The ratio again touched twenty, and stocks began to fall. In terms of gold, we think they have much further to go.

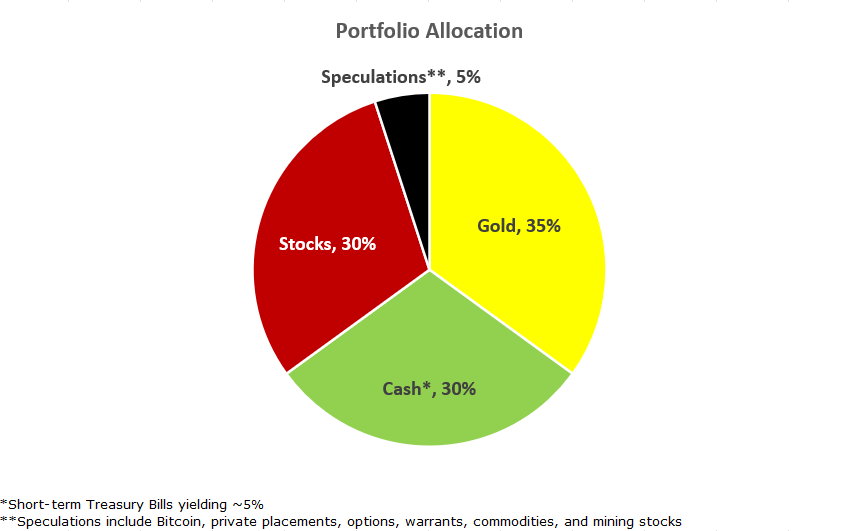

Regardless the ratio (it’s just over 16 now), I think it’s always prudent to own some gold. Certain periods require only a little. Others demand a lot. For my money, this is one of those “others”.

While gold lagged badly during the stock and bond bull of the late twentieth century, that’s not the environment we’re in today. Compared to current astronomic levels, debt twenty-five years ago was relatively low, and real interest rates comparably high. Even after record increases, today’s real rates (based on falsely flattering government data) barely eclipse negative territory!

The point with gold isn’t to increase our wealth. It’s to preserve it. Gold is money. That’s it.

If we endure a crisis, we merely want to retain purchasing power till we come out the other side. We’ve owned gold for years, and (like an insurance premium) never minded its price going down, since that implies most things are going well.

But I don’t think they are. They seem to be getting worse. Within the next few years, it may be time to bar the door and batten the hatches. And gold has always been the best latch.

As storm clouds gather, I’ve increased gold to a third of our portfolio. We’ll keep it there till the Dow-Gold ratio sends a signal to reduce. And then we’ll plan to buy blue chip stocks on the cheap, and ride the dividends the rest of our lives.

Stocks

Jeremy Grantham reminds us that stock markets act “normal” 85% of the time. But it’s the other 15%…when fear, greed, euphoria, or panic are in the saddle to guide the herd… that matter most.

And that’s very likely where we’re about to be. Despite a less rocky path this year, we’re still traversing the greatest bubble of our lives.

For forty years, stocks and bonds charted a lucrative course. A demographic breeze filled their sails, and Fed winds pushed their backs. But after a few years of calm, our forecast is for pressure to shift, clouds to form, and gales to increase.

We’ve seen profitless goofball “growth” stocks that rose on hot air of easy money plummet during the deep freeze of contracting credit. Some have recently bounced. But a large portion will return to earth, and into the grave. And given prevailing financial conditions, even “sturdy” stocks may be part of the wake.

With this in mind, why own stocks at all? Because we must guard against arrogance, and protect against being wrong. And other evidence implies the bull market remains intact.

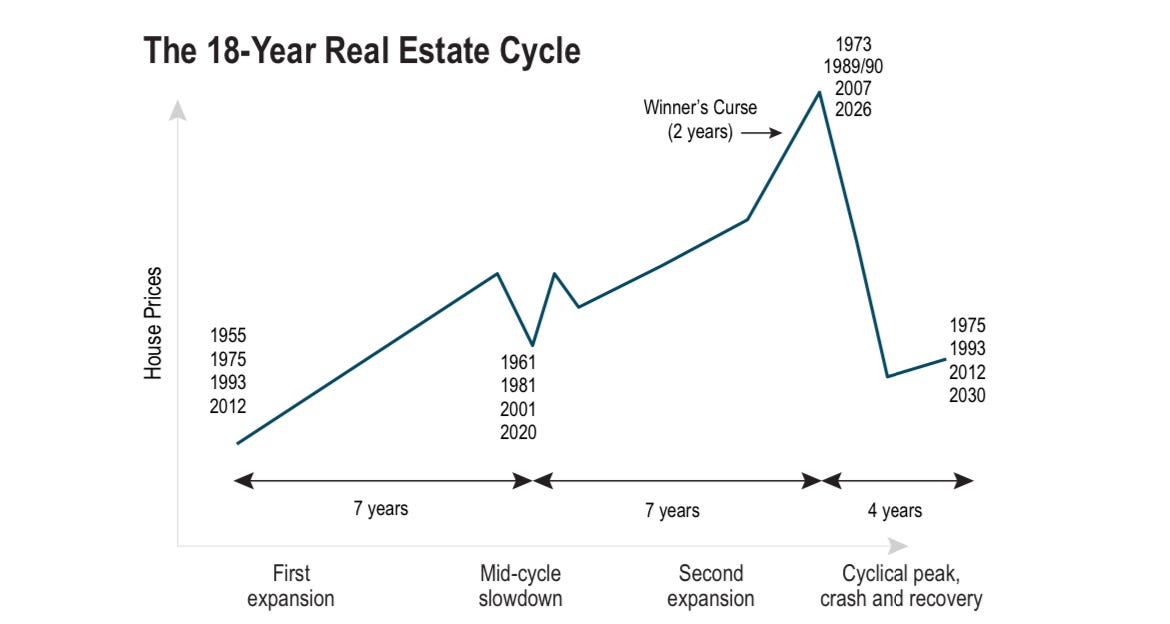

A particularly compelling piece is the 18.6 year real estate cycle, which suggests stocks and land could have a couple banner years before the real decline the middle of this decade. Supported by two hundred years of history, the process is characterized by credit and land values swinging in sync.

Inflating credit pumps up land prices, which act as collateral for the additional credit higher real estate values require. As more credit is granted, land prices keep rising, perpetuating the feedback loop, which carries construction and other real estate related activity with it.

By this pattern, land prices become a leading indicator of broad economic performance. Data reveals peaks every eighteen to twenty years, after which sharp contractions (lasting about four years) inevitably occur. That puts the next collapse (which could cut indexes at least in half) about a year and a half from now.

Will this two-century cycle continue? No one can be certain, especially me. So despite a general aversion (and because the cycle implies stocks should do well the next couple years), owning some stocks is prudent…and an act of humility.

Because something is inevitable doesn’t mean its imminent. No matter when we think stocks may fall, or how far we believe they’ll go (in real terms), we can’t know for sure.

And as we saw in the 1930s and 1970s, some businesses do well when the world is in tatters. Others are strong enough to weather the storm, and prosper when it clears.

These are the type businesses we want to own now. They are solid companies with pricing power, reliable profits, rising dividends, and that produce real things: energy, agriculture, precious metals, maybe some utilities, healthcare, or consumer staples, and the best businesses that ship or store these essentials.

To provide more cushion and extra income, we often sell put options to acquire desired stocks (or enjoy extra income if we don’t). And when selecting them, we embrace concentration by focusing on the best ideas to not dilute performance with over-diversification.

But for the time being our exposure to stocks is greatly reduced, with strict stop-losses for most holdings. As with gold, we should always own some stocks. There are times for more, and times for less.

At our age and risk tolerance…and in this phase of the market cycle…this is a time for less. For regular income and targeted appreciation under anticipated conditions, about a 30% allocation should do the trick. The current holdings in the equity component of our portfolio are included below.

Cash

In inflationary times, cash is a melting ice cube. But, at least for a while, it’ll keep our drink cold while the heat is on. Like a sealed freezer when the power goes out, cash can temporarily preserve the essentials while storm rolls by.

Inflation eats away the value of cash. But when everything else is falling off a cliff, I’d rather float slowly to the ground with the safety of a parachute. That’s what cash provides. It offers diversification, optionality, an ability to sleep, and time to think.

And now, with short-term T-Bills (which is where we’re keeping our “cash”) offering over 5%, we’re being paid to do so. This may change in coming months, at which point we’ll reassess the best place to store our powder.

After markets crash and the smoke begins to clear, cash is the shovel that lets us sift thru the rubble for abandoned gems and overlooked heirlooms. We can use it to scoop up marquee names that few others are able to access. Then, we’ll hold them forever and collect the dividends.

Cash comprises about a third of our portfolio.

Speculations

As we prefaced above, these aren’t times to try to get rich. They’re periods when you diligently try not to become poor. But smart speculation retains a small spot in our anxious portfolio.

I consider Bitcoin less a pure “speculation” than a source of security, or an asymmetric bet that’s likely to pay off. I think it’s the real deal and everyone should own some. But till further notice we’ll stack our small portion in the “speculative” pile.

With it we include an allocation to true speculations like options, warrants, and private investments. In total, and particularly in this environment, we pour into this bucket no more than 5% of investable assets, with strictly limited position sizes based on the risk profile of each holding.

Conclusion

Markets take long trips along winding roads. Accidents are to be expected, with detours along the way. As we’ve seen, major undulations are infrequent, yet come with cyclical regularity.

We don’t know exactly when steep descents will appear or ascents reverse. We have a general idea, and think we’re headed downhill soon. But we don’t know for sure.

Actually…notwithstanding our cycles, charts, hunches, and whims…we don’t know at all. So we adopt the mantra of investment editor Dan Ferris: prepare, don’t predict.

Asset allocation historically affects portfolio performance more than stock selection does, so that’s what I’ve focused on here. It’s more important to be on the right bus than to pick the best seat.

But wherever you sit, be sure to buckle up. To misquote Bette Davis, it’s going to be a bumpy ride.

PORTFOLIO REVIEW

The asset allocation described above and detailed below is what we’re doing with our own money, excluding real estate investments, private placements, warrants, and short-term options trades.

Real estate is very personal and specific to each individual or family (and in many cases is more consumer good than “investment”), so I’ve not included it as an asset class. And options, warrants, and private placements are too risky, illiquid, inaccessible or fluid for me to post anything that anyone reading this might be inclined to act on.

The Ballast

Gold and “cash” are fairly self-explanatory. We’ll hold cash in short-term (less than a year to maturity) T-Bills, at least till yields start to fall (which, as noted above, could be soon). Gold is held in physical form by secure custodians, in allocated storage in other countries, and in redeemable shares in reputable funds. We also hold Bitcoin in cold storage wallets, with keys secured in several locations.

But individual stocks are obviously more specific. Below are the ones we’ve decided to grab, yet are prepared to ditch when risk-adjusted stops are hit: